Summary

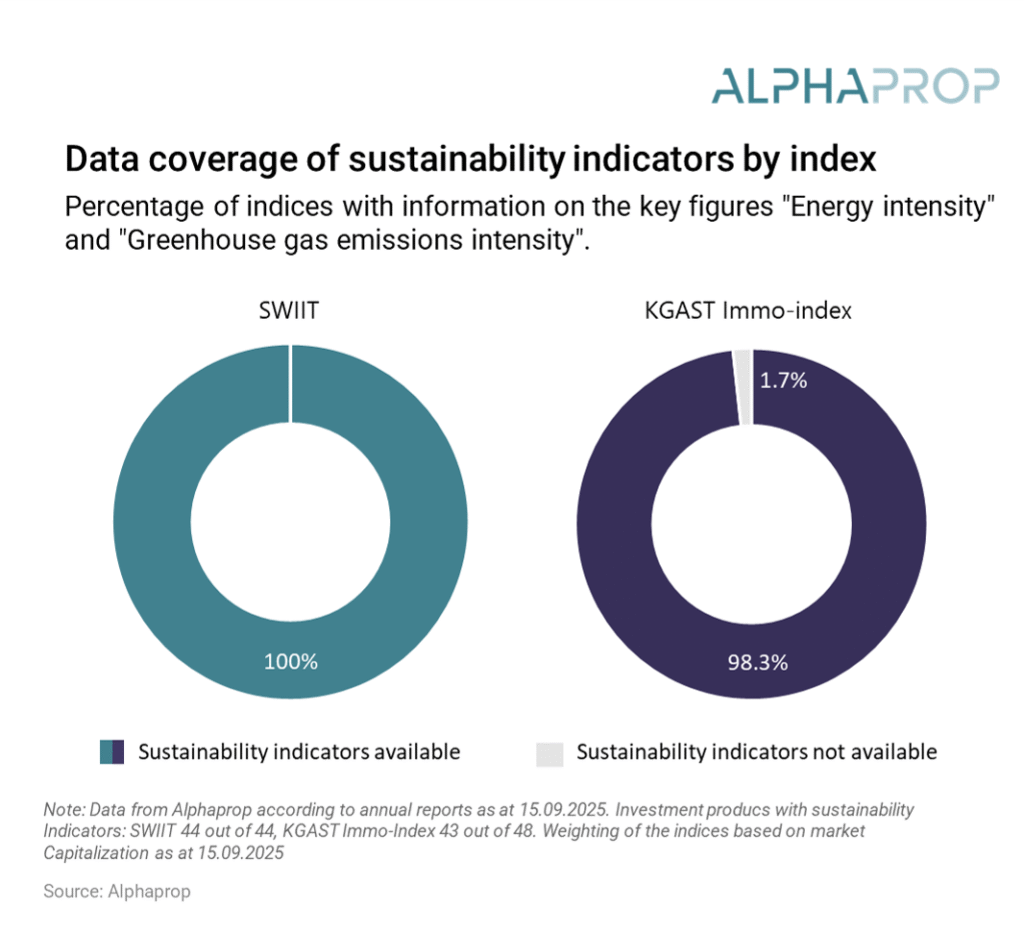

- Since the publication of the AMAS circular on environmental key figures in May 2022, reporting environmental KPIs became the norm. For 100% of SWIIT and 98.3% of KGAST data is available.

- There is a clear methodological convergence to REIDA methodology.

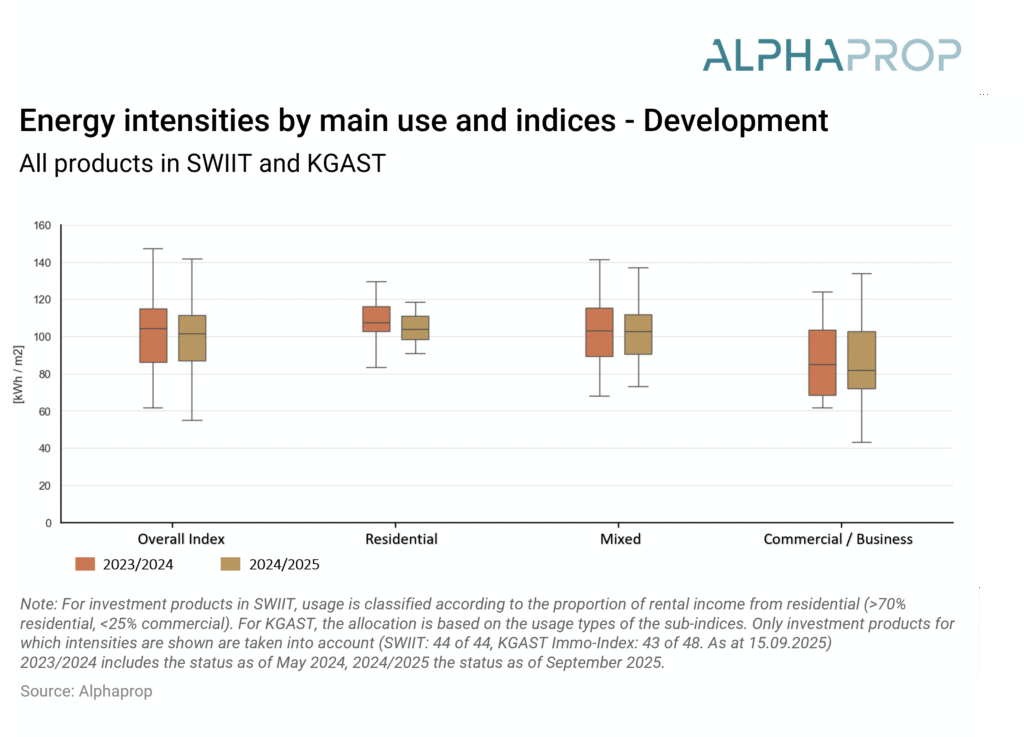

- Both indices have reduced their energy and emissions intensity compared to last year and the share of fossil energy sources was reduced.

- About 70% of the investment products in both indices publish a reduction path with clearly stated targets. On an aggregated level, these paths are aligned with the CRREM 1.5°C trajectory.

- Last year saw a positive reduction in CO2 emissions, aligning with long-term goals. However, the feasibility of implementing the structural measures required for these reduction paths as planned remains to be seen.

The AMAS circular on environmental key figures, published in May 2022, established a framework for standardized sustainability reporting in indirect Swiss real estate investments. This framework was further enhanced by the REIDA CO2-Benchmark, which aimed to increase transparency and comparability across portfolios. Consequently, reporting environmental KPIs for a portfolio is no longer a unique selling proposition, but a fundamental requirement for all real estate asset managers. The new guidelines from June 18, 2025, by the Asset Management Association Switzerland (AMAS), further standardize this process by providing a comprehensive audit framework.

Our analysis focuses on the current state of reporting, with a particular emphasis on the evolution of Swiss real estate funds and investment foundations. Beyond environmental key figures, we examine CO2 reduction pathways and the progress achieved in this critical area.

High data coverage

The guidelines defined within the framework of self-regulation in the AMAS circular require the publication of data points in four categories: coverage ratio, energy mix, energy consumption and its intensity, as well as greenhouse gas emissions and their intensity.

Data availability has improved substantially: ESG key figures are now published for all 44 products in SWIIT and 43 out of 48 products in KGAST, corresponding to 98.3% of the weighted index. This improvement enhances transparency and comparability across portfolios, a core aim of the AMAS circular.

Each year, an increasing number of portfolios are adopting standardized reporting methodologies such as REIDA, which is steadily improving methodological alignment and transparency across the industry. This ongoing shift reflects clear progress toward greater consistency in reporting practices. However, methodological transparency remains an issue, as not all portfolios have transitioned yet – leaving some uncertainty in comparability.

Energy Intensity dependent on usage

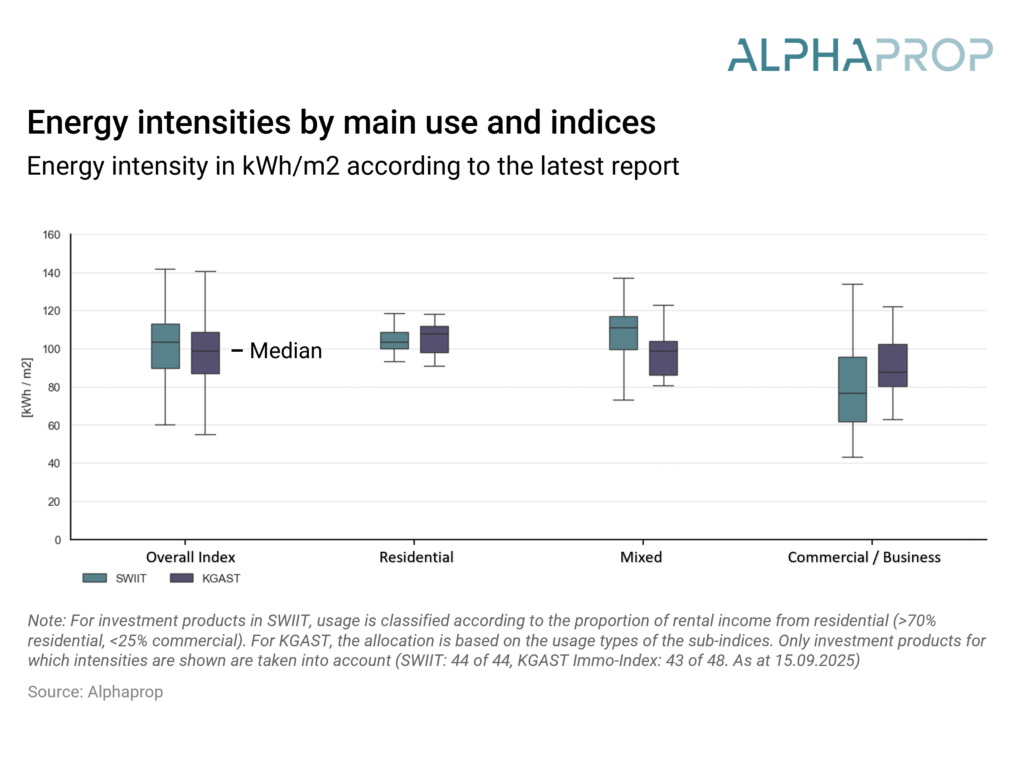

Energy intensity refers to the owner-controlled energy consumed in a building relative to the energy reference area, which also takes into account shared spaces within the property.

The first graph shows that the median portfolio of both SWIIT and KGAST reports an energy intensity of around 100 kWh/m². When broken down by usage type, residential buildings display a higher average energy intensity compared to commercial and other building categories. This largely explains why the overall energy intensity of SWIIT portfolios tends to be higher than that of KGAST, as residential buildings represent a larger share of the SWIIT index.

Compared to last year, both indices show clear progress: energy intensity has declined across all asset types, confirming that portfolios are steadily improving in energy efficiency.

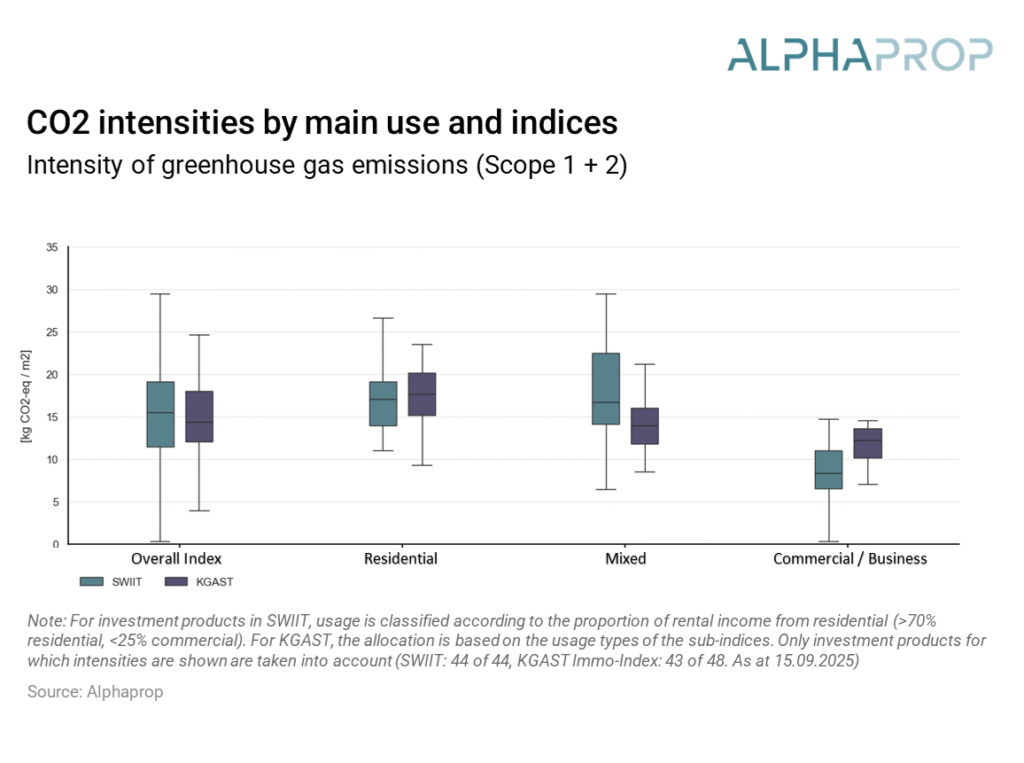

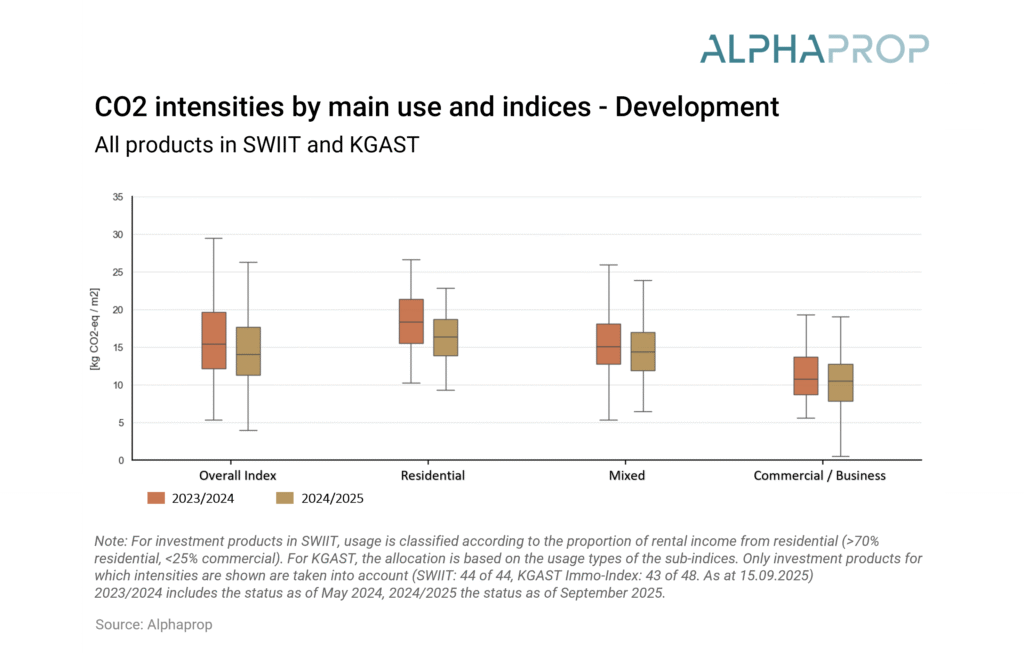

CO₂-intensity slightly reduced

The intensity of greenhouse gas emissions measures CO₂ equivalents per square meter of energy reference area. Following AMAS’s environmental performance indicators, we focus on Scope 1 and 2 – the owner-controlled part.

The following graphic illustrates the distribution of greenhouse gas emission intensity for the two indices, broken down by their primary use.

We can see how CO₂ intensities follow the same path as energy intensities.

In comparison to last year, both indices have achieved a notable reduction in CO₂ intensity: weighted by product, KGAST average value decreased from 14.97 to 13.88 kg CO₂e/m² , and for SWIIT from 16.65 to 14.52 kg CO₂e/m². Whether these reductions are primarily driven by changes in portfolio composition or by shifts in the energy mix remains to be investigated.

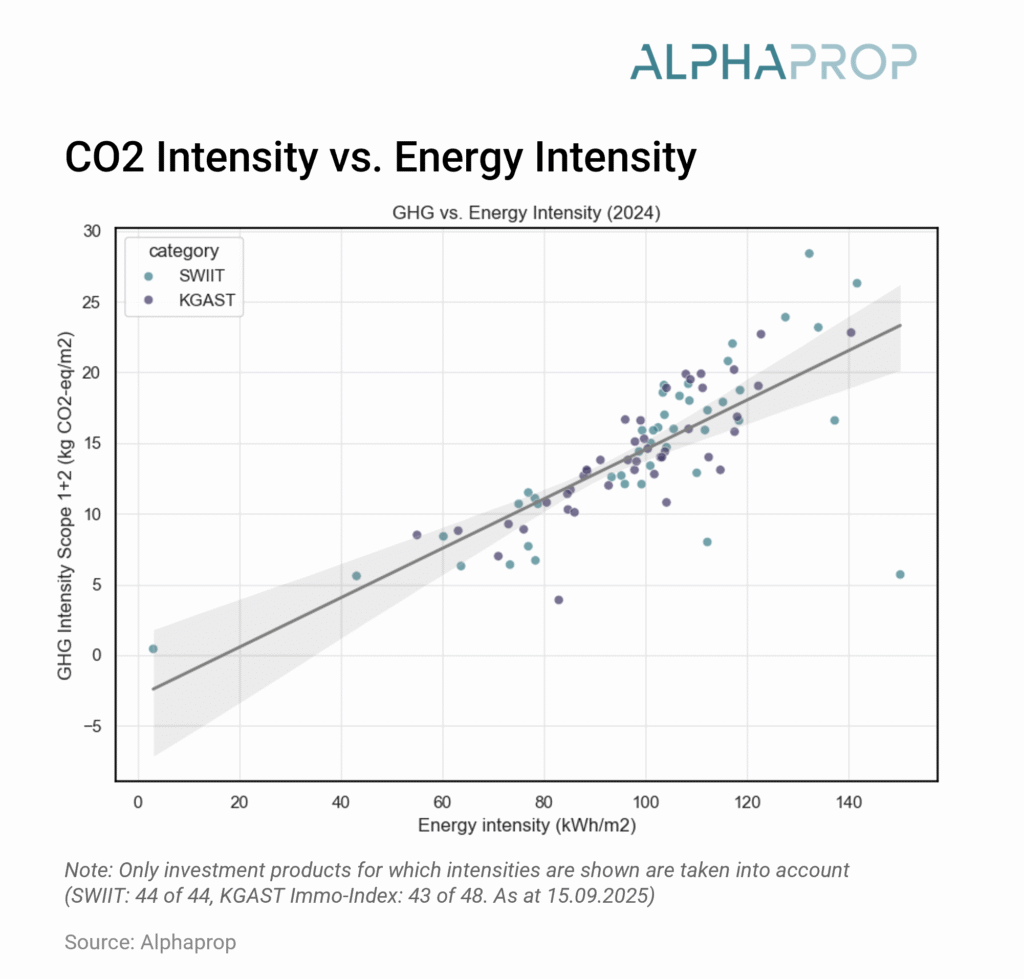

As expected, there is a stable positive correlation between energy intensity and emissions intensity, underlining the importance of energy source selection in determining carbon performance.

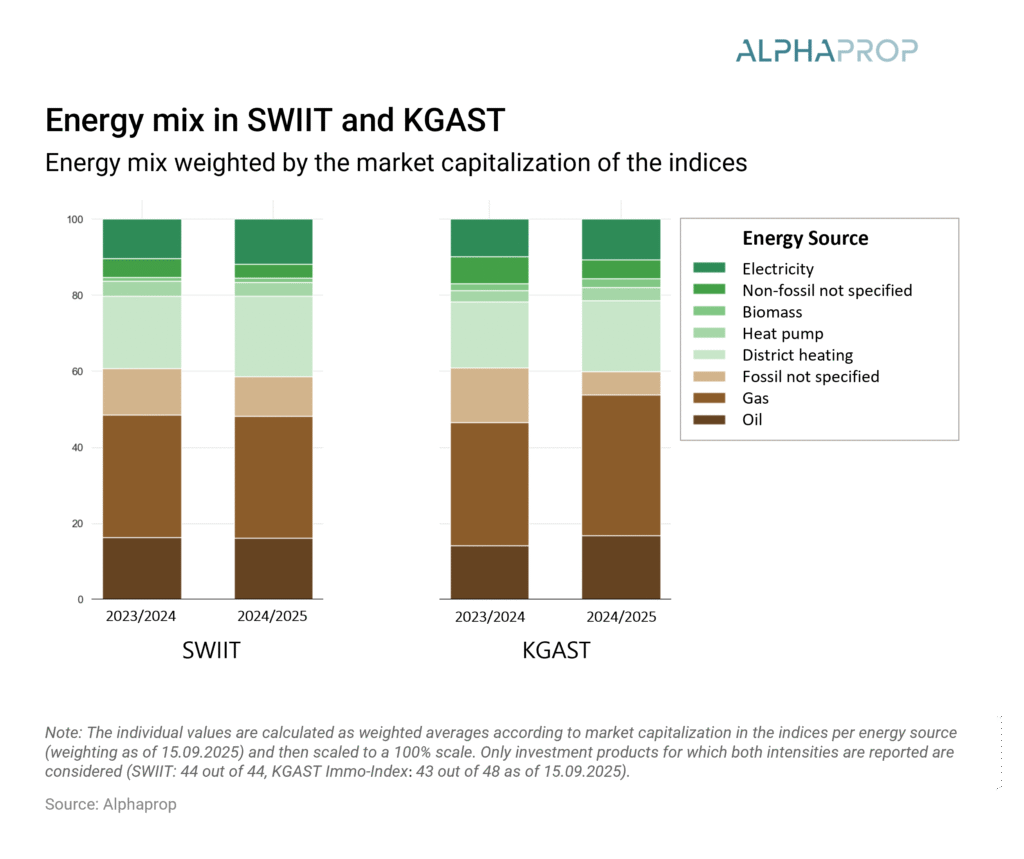

Fossil sources remain main energy source

As highlighted in previous section, energy intensity and CO₂ emissions are closely linked. While reducing energy consumption is one route to lowering emissions, achieving net zero targets requires a strategic focus on transitioning to cleaner energy sources. For this reason, analysing the energy mix is essential. Understanding not just how much energy is consumed, but also where it comes from, enables us to identify opportunities for decarbonization and track progress towards sustainability goals.

Compared to last period, both indices show a modest shift from fossil fuels to cleaner energy sources, particularly district heating. The share of fossil energy, which exceeded 60% in 2023/2024, has now fallen below that threshold for both indices. In addition, the KGAST Immo-Index portfolios have significantly improved the transparency of their energy source reporting: much of the previously unspecified fossil consumption is now more accurately identified as gas or oil.

Other ESG standards are likely to diminish in importance

In addition to the environmental Key Performance Indicators (KPIs) defined by AMAS/KGAST, which build upon the REIDA methodology, there are also ESG benchmarks like the Global Real Estate Sustainability Benchmark (GRESB). These benchmarks aim for a more comprehensive approach, encompassing social (S) and governance (G) components.

UBS’s recent decision to withdraw its Swiss-focused funds and investment foundations from GRESB will likely lead many Swiss real estate asset managers to reconsider their involvement. GRESB is significantly more demanding and broader in scope than REIDA, extending beyond just environmental KPIs.

Currently, 75% of SWIIT’s market capitalization and 61% of KGAST’s market capitalization are GRESB-scored, primarily due to participation of the largest products. However, UBS’s withdrawal is expected to cause a significant 46 percentage point drop in SWIIT’s GRESB-scored proportion, bringing it down to 29%. This reduction is likely to push the share below a critical threshold for the Swiss focused market of indirect real estate.

Given that reporting standards often operate on a “winner takes it all” principle, we anticipate that Swiss investors will primarily demand KPIs based on REIDA methodology as the standard which is also recommended by ASIP. Consequently, asset managers will likely act accordingly and see little incentive for the “extra mile”. The same destiny probably applies to other standards that never managed to reach a significant market share and therefore do not provide clarity for investors.

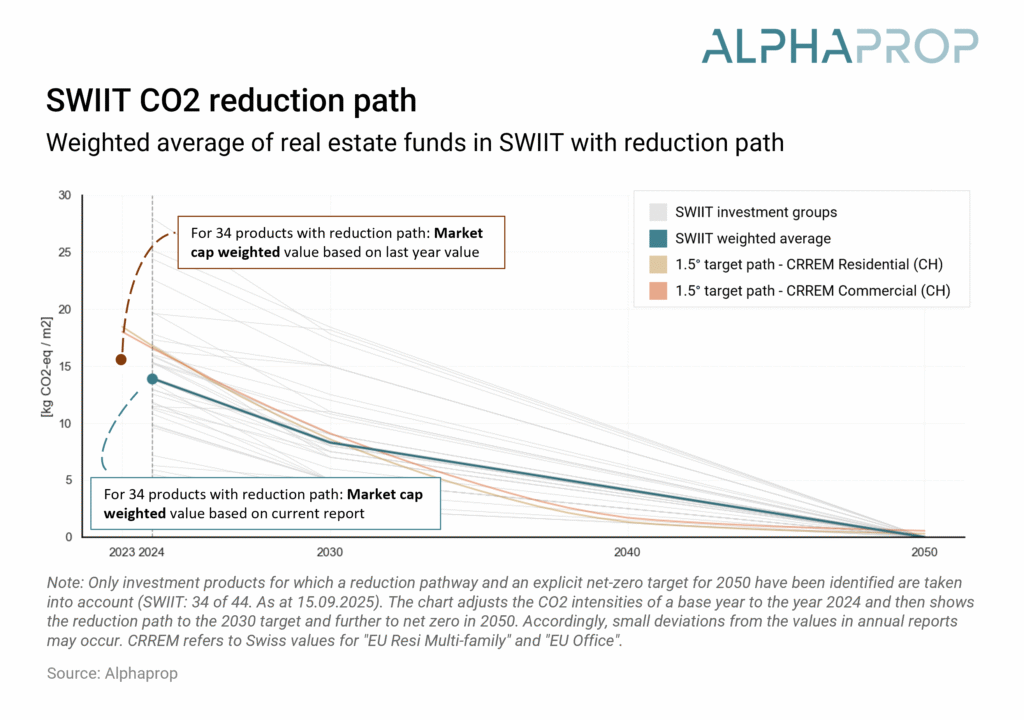

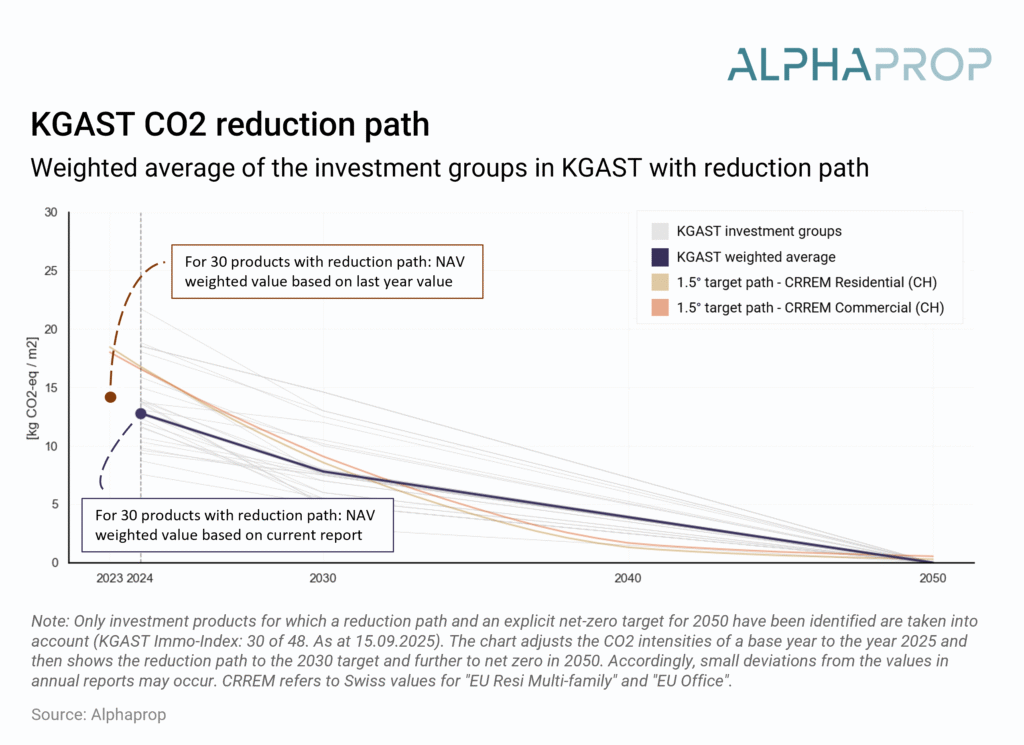

Products on the reduction path

A reduction path illustrates the projected trajectory of greenhouse gas emissions over time, showing how an investment product or portfolio intends to decrease its carbon footprint in line with stated decarbonization goals.

A growing number of investment products explicitly state decarbonization targets:

- Net-zero 2050 is a clearly stated goal for 34 SWIIT funds and 30 KGAST investment groups.

- 2030 interim targets are also common, reported by 36 SWIIT and 28 KGAST products.

As reduction paths are not published in machine readable form, we use these targets to estimate the reduction path. The following graphs show the aggregated reduction paths of SWIIT and KGAST for products that do provide a reduction path – hence it is a subsample of the index.

Both indices show a similar picture: The emissions decreased from last year roughly in line with the reduction path. The reduction paths are in line with targets estimated by Carbon Risk Real Estate Monitor (CRREM) for a 1.5°C pathway. Many portfolios already plan substantial reductions by 2030, which is a promising signal. Compared to last year, both indices remain on average in line with the pathway, highlighting a continued commitment to the announced targets.

Nevertheless, significant differences remain between individual products, and not all have yet published a reduction path. For those without explicit targets, alignment with Switzerland’s climate goals remains uncertain.

Positive development but challenges remain

The 2025 update indicates continued progress in data coverage, methodological enhancements, and quantifiable reductions in both energy and emissions intensity. For products with available aggregated reduction paths, alignment with international climate targets remains largely consistent. A notable positive is that the observed emission reductions are in line with the established reduction path.

Overall, indirect Swiss real estate investments are progressing favorably. Sustained harmonization of methodologies and expedited implementation of structural measures will be crucial for long-term adherence to climate objectives.

Further links

- AMAS Circular (German): Best Practice zu den umweltrelevanten Kennzahlen für Immobilienfonds

- REIDA Methodology (German): REIDA Methodik

- Alphaprop: ESG-Reporting

- CRREM Pathways