For structural reasons, the market for income-generating real estate is not very transparent: properties are rarely traded, each property is unique, and data is scattered among owners, property managers, appraisers, and lenders. Benchmarks based on a reliable data set help contextualize trends, validate assumptions, and make decisions more objective.

Against this backdrop, the REIDA association has launched a total return benchmark as part of a pilot project in collaboration with a group of experts—which includes the SIV—and 13 major real estate owners—as a “benchmark by the industry, for the industry.” Performance is the key economic indicator: It combines current income with changes in value and enables performance to be compared across portfolios and segments—regardless of financing structure or overarching organizational costs.

From the CO2 Benchmark to the Total Return Benchmark

Although REIDA has been active in the field of real estate financial data since 2012, the association has gained widespread recognition in recent years, particularly through its CO2 benchmark. Thanks to close collaboration within the industry, a standard for calculating environmental metrics has been established, which has now been adopted by industry organizations such as KGAST, AMAS, and the Swiss Pension Fund Association (ASIP).

Building on this success, it made sense to create additional comparison options within REIDA’s core area—financial data—and to further enhance the value of the existing database. Since its inception, REIDA has been compiling extensive data from its members. By 2024, the dataset comprised over 3,400 investment properties with a market value of nearly CHF 80 billion across all property types and regions of Switzerland.

By way of comparison: according to pension fund statistics from the Federal Statistical Office, Swiss pension funds held approximately CHF 229 billion in Swiss real estate investments in 2024—roughly half of which was held directly and half indirectly through investment foundations and real estate funds. This scale demonstrates that a very substantial data foundation already exists—and that it will continue to grow in the future as more organizations join.

What is a total return benchmark?

As part of the Total Return Benchmark, information from all participating portfolios—including portfolio master data, land areas, transactions and transfers, year-end valuations, and income statements at the property level (including details on Capex)—is standardized. This harmonizes several thousand income-generating properties with different owners and makes them comparable based on uniform definitions.

The Total Return Benchmark clearly focuses on the Swiss income-generating real estate market—with the aim of providing an industry-wide, consistent, transparent, and practical basis for comparing the performance of existing properties. The focus is not on an organization’s individual balance sheet or financing logic, but rather on the economic performance of the property itself. This requires clearly defined boundaries (e.g., for income, operating costs, vacant properties, and Capex) as well as a standardized approach to one-time items and portfolio changes.

On this basis, a yield to income and a capital appreciation yield can be determined for each property; together, they constitute the total return. In addition, where transactions and transfers have occurred, a return component from purchases/sales is reported. This distinction is important because it highlights different drivers: ongoing earnings power, market- or valuation-driven changes in value, and realized effects from transactions.

REIDA (Real Estate Investment Data Association) is a non-profit organization that continuously improves market data and market knowledge in the field of Swiss real estate investments. REIDA has over 30 members from the real estate industry.

The REIDA Total Return Benchmark is developed together with the pooling agent Alphaprop and 13 pilot organizations. The goal is to create an industry-standard, unified benchmark for the performance of Swiss investment properties.

Alphaprop is the pooling partner for REIDA financial data and conducted the pilot for the Total Return Benchmark.

Impressive average performance

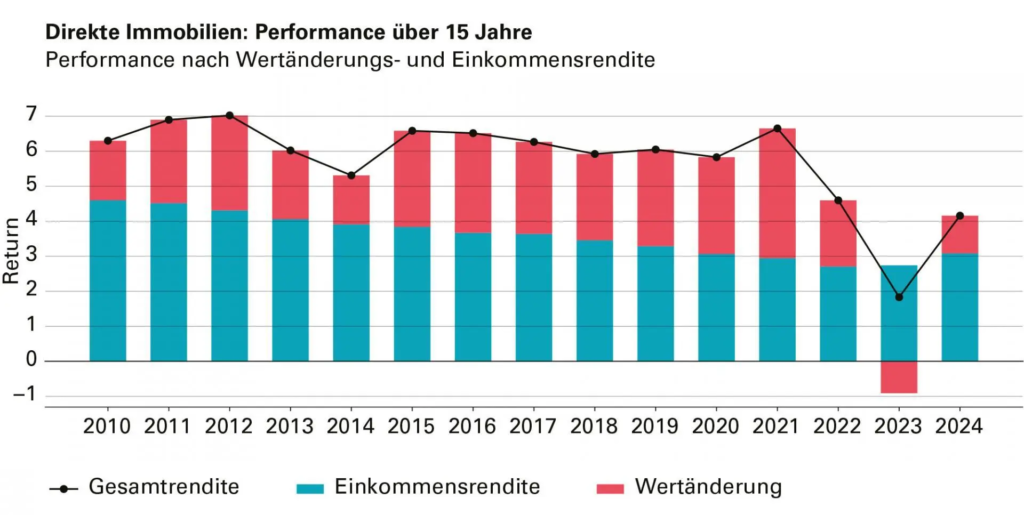

The benchmark data covering 15 years paints a clear picture: Since 2010, the average total return across all property types has been 5.7 percent per year. This figure consists of an income yield of 3.6 percent per year and a capital appreciation yield of 2.1 percent per year. The latter was largely driven by the declining interest rate environment and the associated valuation and discounting effects.

At the same time, there has been a structural shift in the income yield: The annual income yield has declined over time—from an average of 4.6 percent in 2010 to 3.1 percent in 2024.

Over the entire period, the residential sector stood out in particular: with an average total return of 6.2 percent per year, it generated the highest returns. Regionally, the strongest results were seen in the Zurich area and the Lake Geneva region. Core cities in the residential segment, in particular, benefited from the significant reduction in discount rates (see chart).

Comparisons at the portfolio and individual property levels

The Total Return Benchmark enables participating organizations to consistently compare their own performance at the portfolio level against the market—not just as an overall metric, but broken down into income returns and capital gains. The key added value lies in performance attribution: deviations from the benchmark can be broken down into an allocation effect and a selection effect. The allocation effect shows whether performance is primarily driven by which segments are overweight or underweight. The selection effect shows whether the organization outperforms or underperforms the market within its segments.

At the individual property level, properties can be compared with the appropriate benchmark segment, such as “Residential Properties in Central Zurich.” This helps validate valuations and assumptions, highlights outliers, and assists in setting priorities for portfolio management.

An additional benefit is derived from the integration with the REIDA CO2 Benchmark: portfolios that participate in the benchmark can assess CO2 reduction and financial performance together. This makes it clear how decarbonization pathways impact performance and where conflicts or synergies arise between climate and return objectives.

What is important for appraisers?

In a DCF valuation, numerous assumptions are made regarding both revenue and expenses. The benchmark provides a practical reference framework for this purpose, particularly for classifying market rents and rent growth, vacancy rates, and cost components in the relevant segments. This allows for the validation of assumptions without replacing the property-specific analysis.

The Total Return Benchmark is currently still in the pilot phase. The goal is to develop it into a permanent product that offers direct benefits to participating organizations while also serving as a public good for the industry. The broader the data set becomes, the more robust segment comparisons will be—and the greater the practical added value for valuation, portfolio management, and the further development of common standards.

Note: This article was originally publishedin SIV’s “ZOOM” magazine.