Summary

- Since the publication of the AMAS circular on environmental KPIs in May 2022, data availability has been significantly increased.

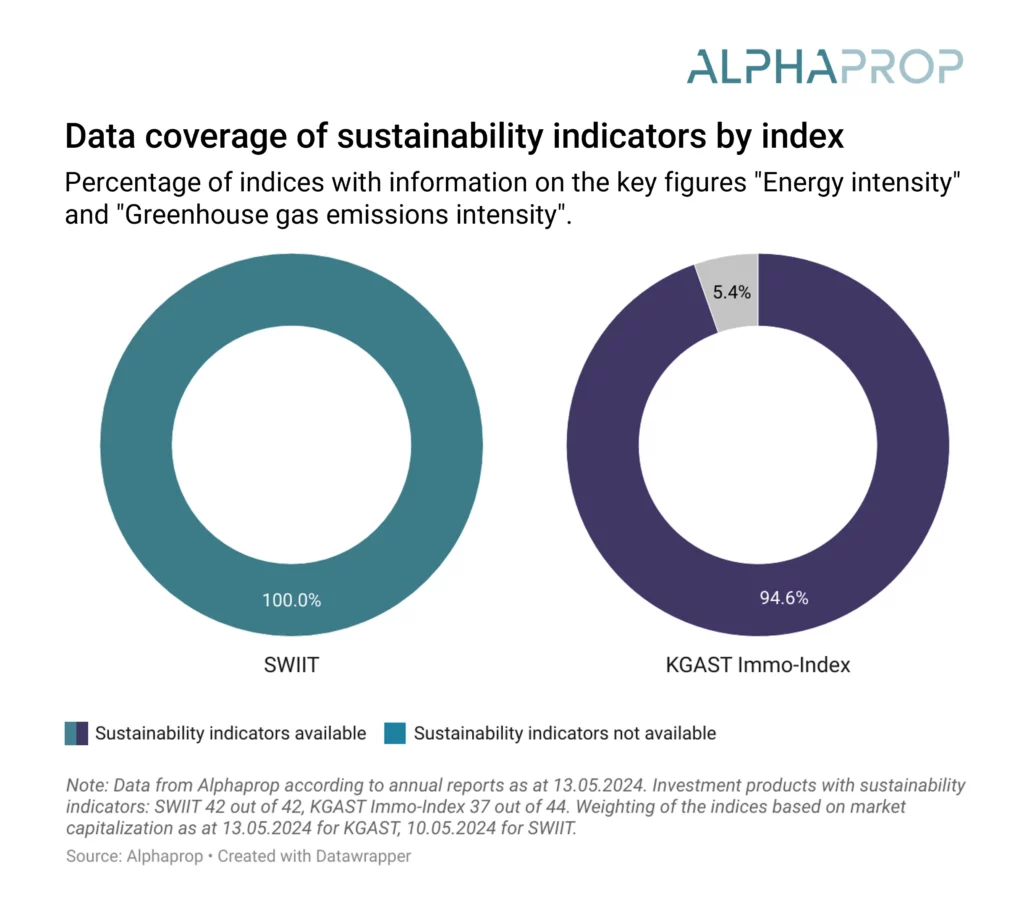

- Weighted by market capitalization, environmental KPIs are available for 100% of the SWIIT and 95% of the KGAST.

- The intensity of greenhouse gas emissions for the SWIIT and KGAST indices is comparable to the current REIDA benchmarks and even slightly below the CRREM target values for Switzerland.

- About half of the investment products in the two indices publish a reduction path. Aggregated, these reduction paths align with the CRREM target paths for a maximum of 1.5 degrees Celsius global warming.

- Whether the necessary structural measures for the planned reduction paths can be implemented as planned will be seen in the coming years.

With the AMAS circular on environmental KPIs, a framework for reporting sustainability metrics for indirect Swiss real estate investments was established in May 2022. The goal is to standardize reporting and increase comparability between portfolios. Over the past two years, the data base and processes for the publication of KPIs have been developed. Against this background, we analyze the current state of ESG reporting with a particular focus on the data coverage of Swiss indices. In addition to environmental KPIs, we focus on the CO2 reduction paths, which will become a central aspect for monitoring progress in the future.

Progress in data coverage

The guidelines defined within the framework of self-regulation in the AMAS circular require the publication of data points in four categories: coverage ratio, energy mix, energy consumption and its intensity, as well as greenhouse gas emissions and their intensity. Data availability was greatly improved with the publication of the annual reports for the year 2023. In the summer of 2023, data coverage was at 89% for the SWIIT and 75% for the KGAST. Since May 2024, ESG KPIs are available for the entire SWIIT portfolio (42 out of 42 investment products) and 94.9% of the weighted KGAST Immo-Index (37 out of 44 investment products). This improved data coverage strictly reflects the availability of information and must be clearly distinguished from the AMAS KPI for “coverage ratio”.

It is important to note that the methods of data collection are often not fully transparent. This makes it difficult for investors to distinguish between actual measurements and modelled data. Additionally, products can only be partially compared due to methodological differences. With the AMAS circular on best practice behaviour, which builds on the guidelines from REIDA, a methodological convergence is likely to occur. The Scope 3 consumption (tenant-controlled emissions), which was not required in the AMAS circular and is also defined as advanced in the ASIP ESG reporting standard, remains a major challenge for most products.

The intensity of greenhouse gas emissions is decreasing

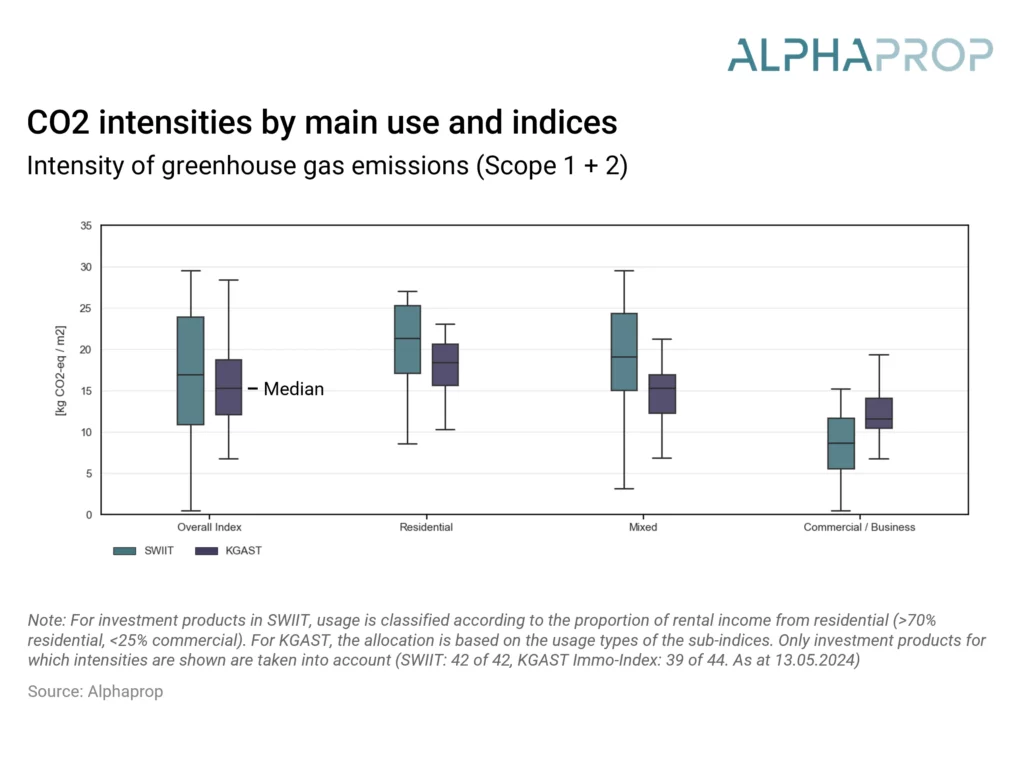

The intensity of greenhouse gas emissions provides insight into the amount of CO2 equivalents emitted per square meter of energy reference area or rentable area. Weighted by product, the KGAST1 records an emission of 14.97 kg CO2 equivalents per square meter. The value of the listed real estate funds index, SWIIT, is 16.65 kg CO2 equivalents per square meter2. These values represent a reduction from the previous year and approach the 2023 REIDA benchmark, which was determined based on 5,290 properties and stands at 13.5 kg CO2 equivalents per square meter. However, changes over time or comparisons with REIDA are only partially interpretable: the measurement times of the reported values vary depending on the investment product and in some cases are over a year old. Moreover, the use of the properties, especially commercial ones, has a significant impact. If properties are largely tenant-controlled and a significant portion of the energy is managed by the tenant, this energy consumption falls into Scope 3 and is not included in the calculated greenhouse gas emissions here. Furthermore, there are likely still considerable methodological differences that will diminish with alignment to REIDA methodologies. Currently, even for knowledgeable readers, it is not clear for many investment products which methodological approach has been chosen.

The following graphic illustrates the distribution of greenhouse gas emission intensity for the two indices, broken down by their primary use.

The portfolios of the listed funds (SWIIT) show a higher median emission compared to KGAST. However, it should be noted that data coverage for KGAST is not complete. There is a possibility that particularly the more intensive emitters have not yet been fully captured, which could distort the overall picture. The type of use of the portfolios plays a crucial role in the comparability of greenhouse gas emission intensity. Investment products that mainly belong to the residential sector exhibit higher greenhouse gas emission intensity. This observation is consistent with the results of the REIDA benchmarking.

First signs of promising reduction paths

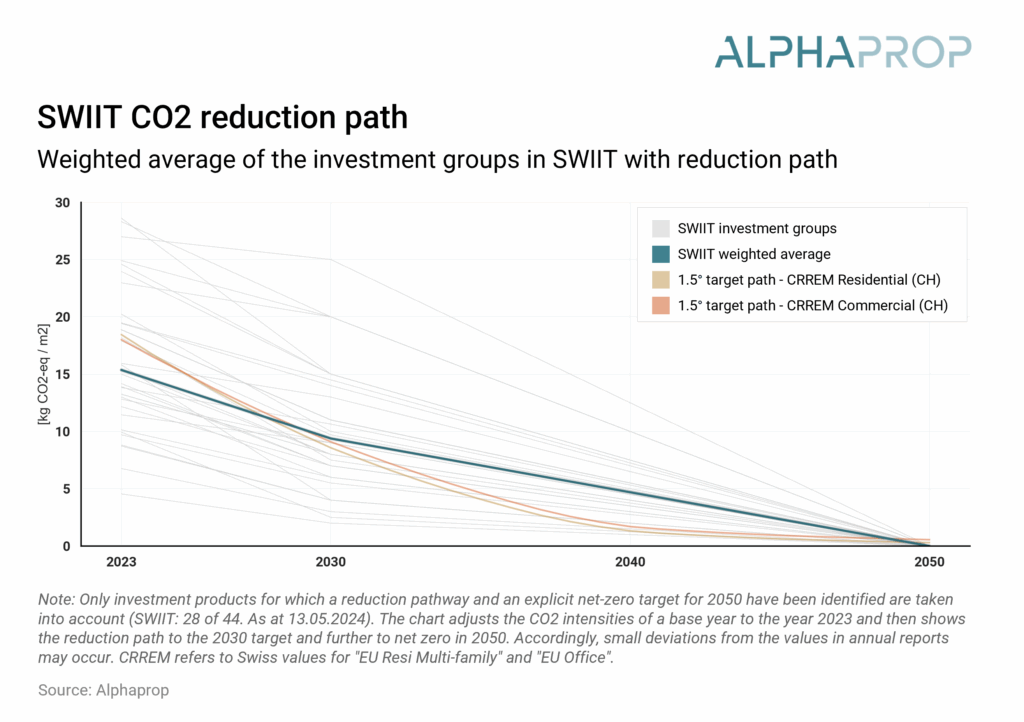

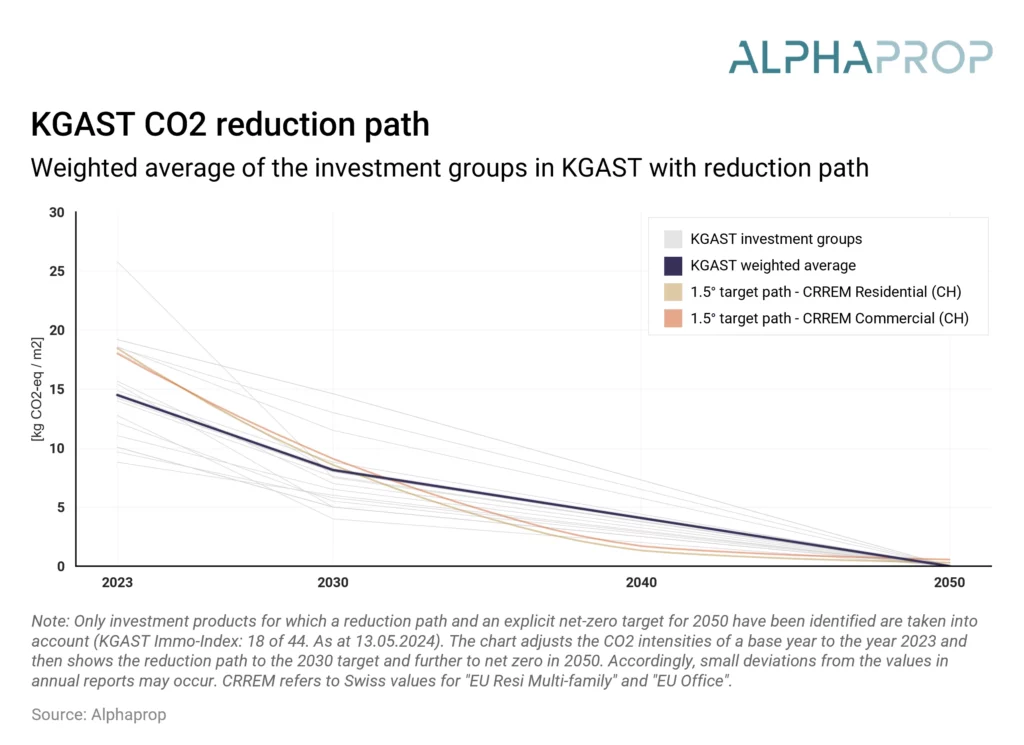

In line with Switzerland’s climate goals, many investment products have set a target of achieving CO2 neutrality by 2050. This is explicitly stated in the annual reports of 31 real estate funds in the SWIIT and 24 investment groups in the KGAST. Slightly more common are CO2 targets for 2030, which have been defined for 33 and 24 products, respectively. Based on these targets and other data in the sustainability reports, initial overarching estimates of reduction pathways can be made. These estimates enable investors to compare actual progress with planned trajectories.

We start from the current value or initial value of the product’s reduction path and, for simplicity, extrapolate linearly from the initial value to the target value for 2030 and to net-zero in 2050. The available reduction paths are aggregated with the respective weighting in the index to form an “index reduction path.” In the next two graphics, these paths are visualized for the two indices.

The graphic shows various paths for reducing CO2 emissions, measured in kilograms of CO2 equivalents per square meter (kg CO2e/m²), over the period from 2023 to 2050. Each gray path represents a product of the respective index. Generally, the reduction paths show a clear trend toward reducing CO2 emissions over the entire period. Both KGAST and SWIIT are performing well compared to the 1.5-degree target paths of CRREM as of 2023. However, there are significant discrepancies between individual products. Additionally, it is assumed that the reduction path, especially for products that have not yet published one, presents a major challenge.

Thus, the newly available data provides a good overview of the initial situation for indirect Swiss real estate investments. The level of emissions is even slightly below the CRREM reference value. Whether the necessary structural measures for the planned reduction paths can be implemented as planned and whether these costs are already fully reflected in today’s valuations will become apparent in the coming years.

Endnotes

1 The KPI is available for 39 investment products

2 Contains the last published value (can therefore include different times of the measurement)