Summary

- Solid performance: Over twelve months, listed real estate funds are at 7.77 %, real estate shares at 12.67 % and the KGAST (NAV) at 5.06 % – all indices positive YTD.

- Investment returns: 5.1 % on average (57 products, CHF 62 billion), with residential products benefiting strongly from valuation gains and commercial products from higher operating returns.

- Record capital inflows: CHF 3.7 billion in capital increases announced or completed for 2026 – new record at this time.

- Growing political risks: The Zurich housing protection initiative (June 14) and an impending tightening of the Lex Koller law signal that the regulatory hurdles for indirect real estate investments will tend to become higher in the future.

The market for indirect Swiss real estate investments remained relatively solid in operational terms at the end of May 2026 despite various emerging challenges. Since the beginning of the year, all indices closed in positive territory at the end of May. Over twelve months, the performance of listed real estate funds is 7.77 % and that of listed Swiss real estate shares is 12.67 %. At 5.06 %, the KGAST index, which is valued at NAV, is just in line with the average long-term annual performance of the last 20 years. Accordingly, the premiums on listed investments remain high. After a brief dip in March, the adjusted premium on the SWIIT is back above 34%.

Discount rates: Slightly falling again

The first investment products with closing dates at the end of Q1 have already been published. Nevertheless, here is a brief look back at products closed at the end of the year – by far the largest balance sheet date. The median discount rates for the portfolios closed at the end of 2025 were slightly lower (-6 bps).

Investment returns: Residential with capital gains, Commercial with operating performance

The clearly positive investment returns are definitely back. The following chart shows the investment returns of all funds and investment foundations at the end of the year. This comprised 57 products with net assets of CHF 62 billion. The average investment return was 5.1 %. Of this, 3.13 % was attributable to net income and 1.85 % to capital gains (0.12 % to other changes in net assets).

Methodology used to present the investment return

The chart shows the investment return of all real estate funds and investment foundations with a focus on Swiss real estate that close their financial year on a defined balance sheet date (30.09; incl. products closing on 31.10) and whose data was published and available at the time the analysis was prepared.

The investment return is divided into a component from the net income and a component from the capital return. The respective portions are calculated per unit on the basis of the change at the end of the year. In the event of capital increases, income from the sale of units and allocations/withdrawals of depreciation that affect net assets, a residual value may arise, which we report separately.

The chart represents a snapshot of the current market environment and does not constitute an investment recommendation.

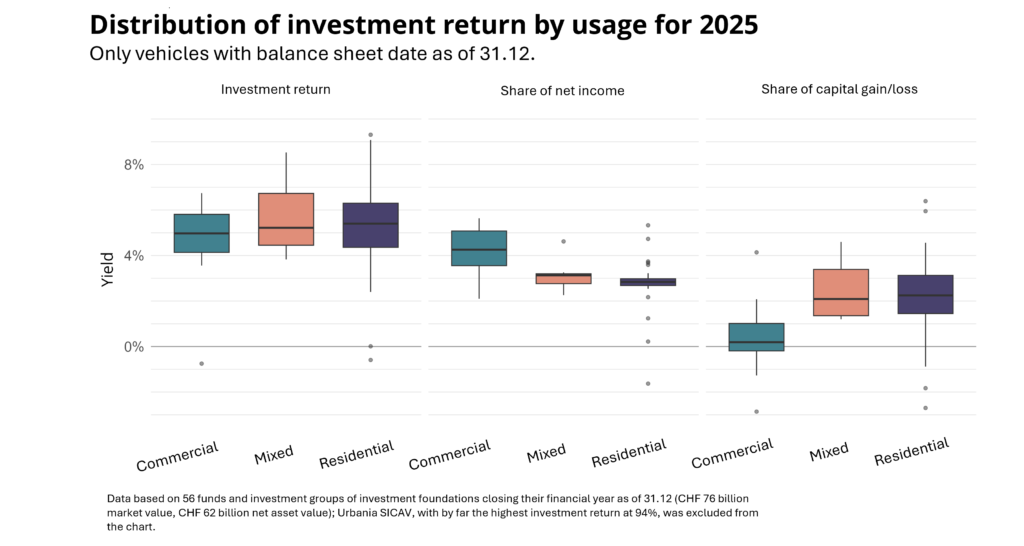

The difference by use is striking: residential products achieved a median of almost half of the investment return through valuation gains, while commercial products show only minimal appreciation, but a significantly higher operating return. The following chart shows the distribution of the investment return and its components as a box plot. The median investment return for residential products was 42 bps higher than that of commercial products (5.4 % vs. 4.98 %).

The Alphaprop data portal supports the analysis and comparison of indirect real estate investments

- Clear, intuitive dashboard for the entire universe of indirect real estate investments in Switzerland

- Used by leading asset managers, pension funds, consultants and product providers

- Over 170 products with over 180 billion net assets

- Analysis option down to individual property level (over 9,500 properties)

- Create clear product comparisons and benchmark reports in PDF format

- Upload your own indirect or direct portfolio and asset-weighted presentation

Interest rate uncertainty, capital inflows and political risks

In view of global uncertainty and the high oil price, the question arises as to the extent to which inflation in the USA and Western Europe could continue to rise and – despite the strong franc – also drive inflation in Switzerland. The 10-year CHF swap rates as a measure of interest rate expectations have risen slightly in recent months. Listed real estate investments are correspondingly sensitive to this change.

Despite the rather uncertain environment, real estate funds are busy raising capital. As at the end of May, capital increases totaling CHF 3.7 billion had been announced or already completed for 2026 – a new record at this point in the year. In 2025, the volume of funds was CHF 4.9 billion. In funds with a clearly positive premium, the capital is always subscribed as the new units are issued at NAV (plus fees). By contrast, a listed fund with a premium of around 0 was no longer able to fully subscribe – potentially an initial signal of restraint and, at the current premium level, a preference for investment foundations. Following a capital increase, the question arises as to how productively investments can be made on the current transaction market, particularly in the case of residential products. The possibility of investing in one’s own portfolio is certainly an advantage here.

Real estate investments are operating in a political environment that has probably never been so harsh for real estate investors in recent years. The housing protection initiative of June 14 in the canton of Zurich represents the high point for the time being. Its acceptance would have a clear impact on indirect real estate investments. According to our analysis, over 10 % of SWIIT’s market values are in residential or mixed-use properties in the canton of Zurich, which would probably be affected by additional regulation. However, even in the event of a “no” vote, further proposals will follow in various regions. A tightening of the Lex Koller is also on the table, which would massively intervene in the market for commercial investment properties and indirect real estate investments. While the current proposal is quite far-fetched and its consequences would be devastating, we assume that adjustments or weakening will follow. Nevertheless, this is also a signal that the hurdles for players in the field of indirect investments will be higher rather than lower in future.