Summary

- Timothy Frei, ESG Product Owner at Alphaprop, explained that auditable sustainability figures are only possible with a consistent, transparently documented data process.

- Thomas Spycher, Partner at Alphaprop, pointed out that the publication of environmentally relevant KPIs has now become firmly established in the market thanks to standardization.

- Stephan Artus, Senior Business Counsel at the Asset Management Association Switzerland, explained how the auditing of environmentally relevant KPIs fits into the AMAS self-regulation and which transition periods apply.

- Remo Satta, Managing Director of Resa Business Audit, explained how the auditing process works and that early preparation is essential.

The publication of environmentally relevant KPIs in accordance with the AMAS/KGAST guidelines has established itself as the standard in the indirect Swiss real estate market. The industry is now facing one of the most significant changes in this context: in the annual reports of real estate funds from the publication date of December 31, 2028, all environmentally relevant KPIs must not only be published, but also audited.

In our last Alphaprop Insights webinar, experts shed light on the new regulatory requirements and the process for calculating auditable ESG KPIs.

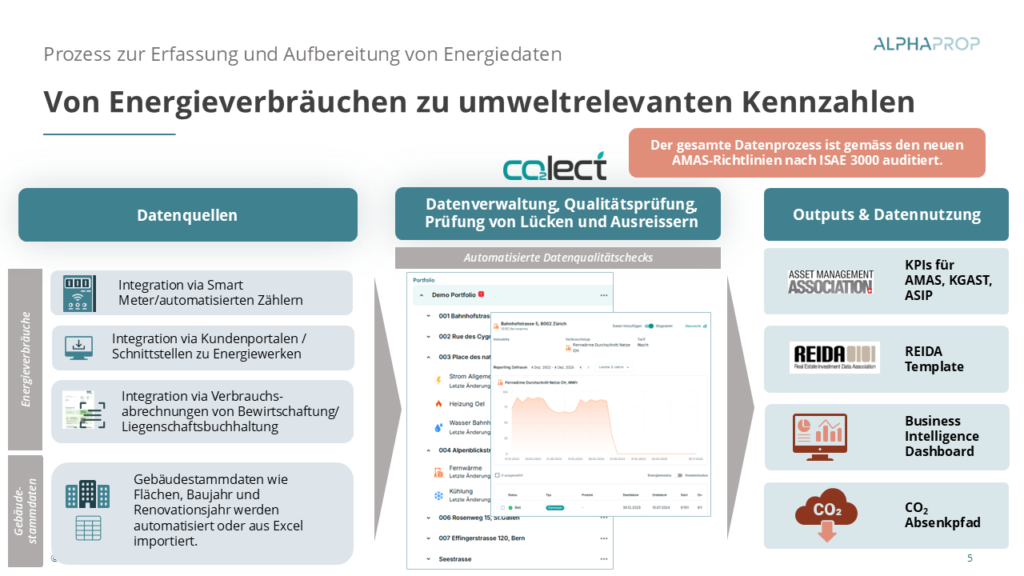

From energy data to auditable KPIs

Timothy Frei (Alphaprop) pointed out that every ESG KPIs is ultimately only as reliable as the foundations on which it is calculated. In order to meet the stringent requirements of an external audit, data flows must be seamless, transparent and traceable from the outset. At Alphaprop, the co2lect data collection platform serves as the technological basis for this, where all data from different sources is integrated, harmonized and checked for quality.

The data process is divided into the following steps:

- Flexible data integration: co2lect enables the direct integration of automated meters as well as direct interfaces to the portals of the energy companies.

- AI-based data collection from bills: Traditional consumption bills do not have to be typed in manually, but are read out fully automatically using an AI-based algorithm and integrated into co2lect. This increases quality and reduces the time required.

- Seamless audit trail transparency: For subsequent verification, each data point in co2lect is linked to the original source (e.g. invoice) so that the origin can be traced with absolute transparency.

- Automated quality check: Automated plausibility checks are carried out directly during data import. This shows where there are gaps in the data or where there are outliers that need to be checked and, if necessary, corrected.

After a successful plausibility check, standardized KPIs can be calculated in accordance with the REIDA standard, the data can be prepared in user-friendly, interactive BI dashboards or CO₂ reduction paths can be simulated.

Alphaprop supports owners in collecting energy data and preparing it for REIDA data entry

- Collection of energy data (e.g. automated reading of invoice data using AI)

- Calculation of environmentally relevant KPIs according to AMAS/KGAST

- Preparing the data for participation in the REIDA CO2 benchmark (filling the REIDA template)

- Calculating the CO2 reduction path on the basis of a refurbishment plan

- Preparation of the data in an interactive analysis dashboard

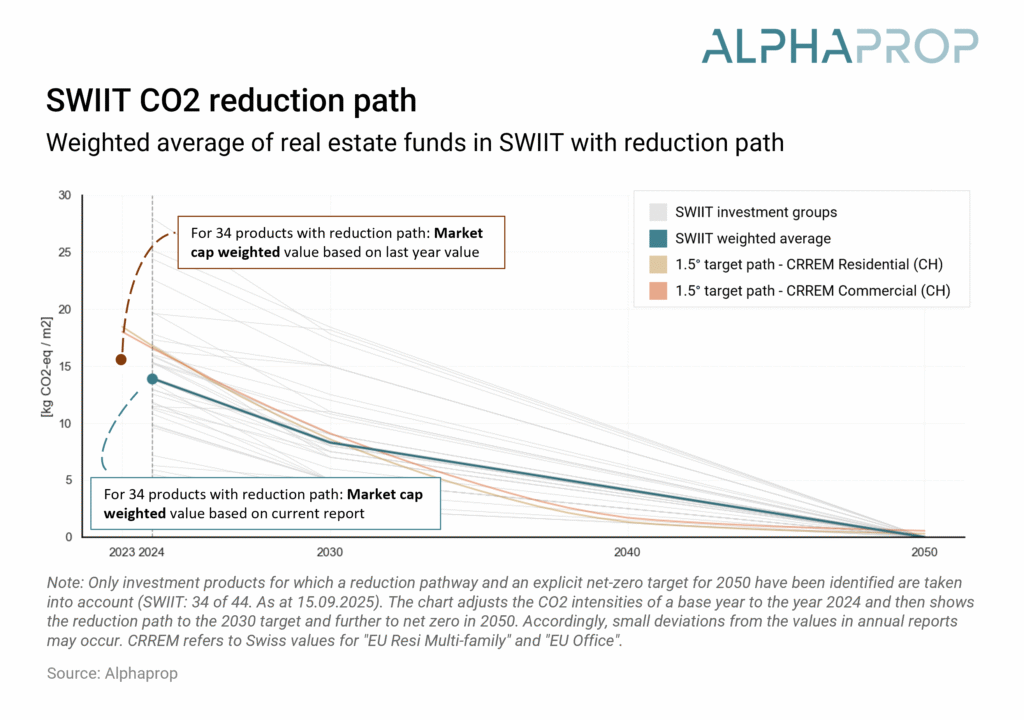

Market analysis: Indirect real estate investments on a downward path

Thomas Spycher (Partner at Alphaprop) gave an in-depth overview of the ESG development of the indirect Swiss real estate market. In 2021, the complete analysis of environmental indicators was still a challenge, as many vessels did not report any data or followed completely different standards. This changed fundamentally with the AMAS circular of 2022, which formed the basis for today’s environmentally relevant KPIs and contributed significantly to the standardization of ESG reporting.

Today, the key environmental indicators are firmly established in the market:

- Coverage: The percentage of the portfolio area (energy reference area) for which data is effectively reported.

- Energy source mix: The breakdown of total energy consumption into individual energy sources such as oil, gas or district heating.

- Owner-controlled consumption: The energy required in operation for Scope 1 and 2 – i.e. explicitly excluding purely tenant-controlled energy.

- Energy and greenhouse gas intensity: The comparative figures (e.g. kilowatt hours or tons of CO₂ equivalents per square meter and year) that allow comparability across portfolios of different sizes.

The analysis shows a high level of coverage: in the SWIIT index, 100% of products now publish corresponding environmental key figures, and almost the entire market also follows suit in the case of investment foundations (KGAST). Over 80% of products also explicitly state that they follow the standardized REIDA methodology.

The data enables investors and asset managers to make valuable comparisons. For example, commercially used portfolios often show lower median CO₂ intensities per square meter than residential portfolios, which is due to the specific use and the definition that tenant-controlled emissions are excluded from these KPIs. Overall, the index-weighted market trend for the reduction paths is already pointing steadily downwards.

New AMAS guidelines for auditing environmentally relevant KPIs

Stephan Artus (Business Counsel at AMAS) explained the background to the new auditing obligations for environmentally relevant KPIs. The independent review by third parties is not in the association’s own interests, but is an explicit requirement of the Federal Council to prevent greenwashing in the financial sector.

The requirements were further specified with the self-regulation revisions adopted last year.

- Article 3 clarifies that the pure approaches of exclusion criteria, ESG integration or the mere exercise of voting rights are not sufficient, either individually or in combination, to qualify a product as “sustainable”.

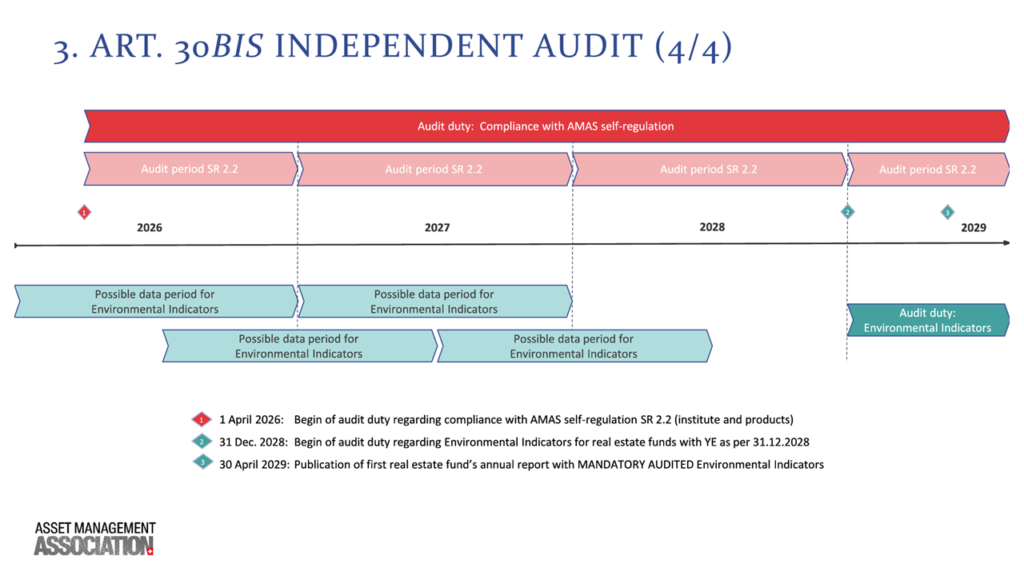

- Exceptions & transitional periods: For existing real estate funds licensed by FINMA, transitional provisions apply until December 31, 2028.

Why does the audit obligation for environmental indicators not apply until the end of 2028?

Many market participants are wondering why the obligation to audit environmental indicators only applies to annual reports with a reporting date on or after December 31, 2028. Stefan Artus justified this with the considerable time lag in the collection of consumption data.

While financial figures are available quickly after the end of the year, the collection and preparation of energy bills often takes more than half a year. As billing periods for properties often differ from the calendar year (e.g. 1 July to 30 June) and funds must publish their reports no later than four months after closing, the environmental reports shown always lag a year behind the financial data in organizational terms. In order for audited data to be available for the annual report at the end of 2028, data providers must be able to set up fully auditable data structures as early as January 1, 2027. From today’s perspective (May 2026), providers therefore only have a good six months left to make their controls and processes “fit for audit”. Under supervisory law, the depth of the audit is designed as a limited assurance review in accordance with ISAE 3000.

The auditing process: perspectives and stumbling blocks from practice

Remo Satta (owner of Resa Business Audit) provided practical insights into the specific procedure for an audit. The ISAE 3000 limited assurance audit is not a 100% full audit of the sustainability report, but a sample-based audit with limited assurance (= limited assurance). The objective is to confirm that the KPIs reported are essentially correct and free of material errors.

The typical audit process comprises four phases:

- Audit planning: Understanding the business model and precisely defining the scope of the audit. Resa recommends carrying out a voluntary pre-audit based on data from the previous year. This allows documentation gaps to be identified at an early stage without legal risk.

- Assessment of processes and ICS: The auditors check how consumption data is recorded, entered into the system and converted into greenhouse gas emissions using emission factors. They also check whether internal control systems (ICS), guidelines and quality checks (dual control principle) exist and are consistently applied.

- Audit procedures (substantive testing): Targeted random samples are taken and the calculations are recalculated completely independently (re-performance). This is supplemented by analytical deviation analyses in the event of significant portfolio changes.

- Reporting: The final product is the formal assurance report. Customers also receive an internal management letter containing valuable best practices and optimization potential for the process landscape.

According to Remo Satta, three key stumbling blocks regularly emerge from audit practice:

- Inadequate data delimitation: Regulatory definitions are often mixed up – for example, due to incorrect scope allocation of tenant electricity versus general electricity.

- Undocumented extrapolations: If data gaps have to be bridged by estimates, heating degree day or climate corrections, the mathematical models behind them are often inadequate or not documented at all. For an auditor, however, what is not documented cannot be audited.

- Lack of historical consistency: In the case of portfolio acquisitions or changes to calculation methods (e.g. adjustments in the Greenhouse Gas Protocol), the previous year’s values are often not corrected. This leads to “apples and oranges” being compared over time.

Conclusion

The auditing obligation from the end of 2028 may still seem a long way off at first glance, but the organizational schedule is extremely tight. As error-free recording and documentation must be in place by January 2027, fund management companies and asset managers should make intensive use of the coming months. Transparent data processes, such as those offered by Alphaprop, and voluntary pre-audits offer the ideal opportunity to raise data quality to an audit-proof level in good time.